The concept of renting out unused equipment is a popular and growing trend for many businesses. By renting out unused equipment, companies can increase profits, access specialized equipment, save time and money on maintenance, and maximize their resources. In order to do this, you need a high-quality equipment rental agreement, and the best way to create one is by downloading our equipment rental agreement template.

For expanding businesses or needing access to specialized equipment, renting out unused gear can be an attractive option. By leasing equipment, companies can avoid significant capital expenses, access the newest technological advances without incurring high purchase costs, and strategically obtain specialized tools that they may need the representation of within their own inventory.

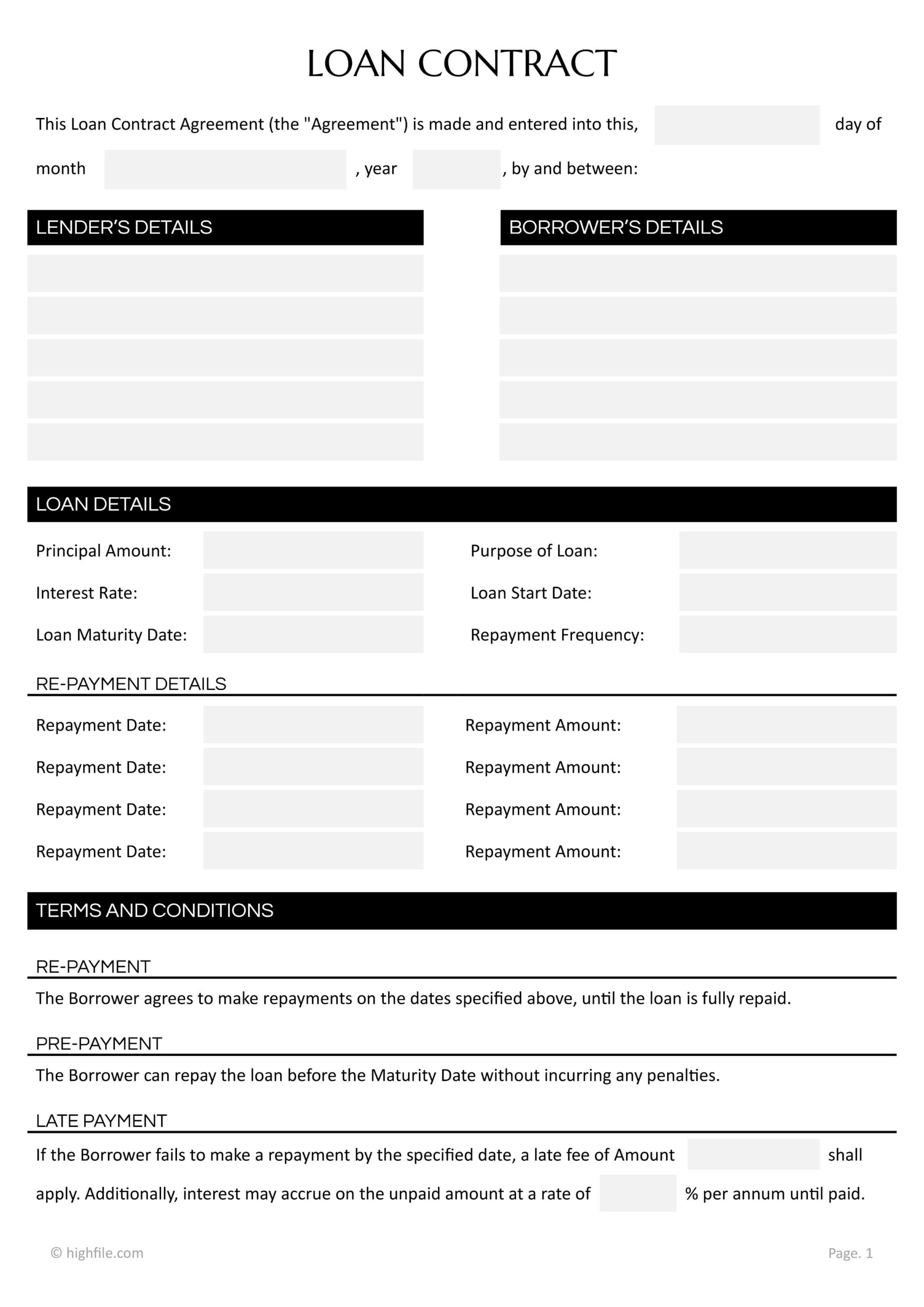

What Is an Equipment Rental Agreement?

An equipment rental agreement is a legal document between a person or business renting out equipment and the person or company reserving the equipment for a designated period. This agreement outlines the terms and conditions under which the equipment will be used, as well as any restrictions, limitations, and responsibilities related to the use of the equipment. Depending on the parties involved, this equipment rental agreement may require a deposit or other form of payment in advance. These agreements are usually written in consideration of both parties and protect each party’s rights to use or lease the equipment.

What Is an Equipment Rental Agreement Template?

An equipment rental agreement template provides you with the framework for crafting a well-written legal document. Using a template helps save time and write an efficient, effective, complete form. These templates are simple to download and modify. Moreover, they are reusable and take only moments to update with new information. They are compatible with most writing programs like MS Word, Excell, and OpenOffice.

Essential Elements of Equipment Rental Agreement Template

- Business Name and/or Logo- Put this at the top of the page to identify the owner or company leasing out equipment.

- Form Title- The title is always in large, bold print and should state that this is an “Equipment Rental Agreement.”

- Rental Company Contact Information- Basic information such as the address of the main office and email goes here.

- Owner Information- The owner’s full legal name, along with their address, phone number, and email, belongs here.

- Renter Information- The full legal name of the renter, along with their address, phone number, and email, belongs here.

- Equipment Information- This should be a chart with the equipment name, description, number of items, and serial number listed for each rental.

- Equipment Value- Include the total value of the equipment.

- Rental Information- Rental information should include all the rental details, such as the start and end dates, monthly cost, deposit amount, and payment due dates.

Terms and Conditions (Page 2 of Rental Agreement)

- Parties- This states that the named parties, owner, and renter have agreed to the lease of the above equipment.

- Duration- The duration states the beginning and end date, the fact that the lease automatically terminates upon ending, and any option for extending the lease.

- Payment Information- Payment information restates the cost and fees, payment due dates, and total value.

- Rights and Obligations- This section details what the equipment can be used for, who is responsible for its upkeep, repairs, transportation, and other vital details.

- Security Deposit Terms- The terms for the security deposit typically state the amount and when/whether it is refundable.

- Insurance- The terms belong here if either company is required to carry insurance.

- Additional Agreements and Information- Additional agreements can include many different things, such as whether the contract can be amended, by whom, and for what purpose, penalties for failed delivery, fees for late returns, severability, and governing laws.

- Date- This is the date that the agreement is signed.

- Owner Signature Line- Signatures are the legally binding portion of the agreement. The owner signs their consent to the terms here.

- Renter Signature Line- The renter signs their consent to the terms here.

Pro Tip: Many businesses that own equipment rent it out seasonally or when it’s not in use to add to their profits. Regrettably, this can limit the availability but also gives access to advanced equipment to individuals and businesses that would otherwise not be able to afford to purchase the equipment for themselves outright.

The Importance of a Well-Written Equipment Rental Agreement Template

The importance of a well-written equipment rental agreement template cannot be overstated. It ensures that both parties understand their rights and responsibilities and helps to protect both parties in the event of a disagreement or dispute. The agreement should clearly outline the rental period, payment terms, late fees, insurance requirements, and other essential details. A template prevents misunderstandings or accidentally missed information and makes sure that both parties know what they are getting and what they are obligated to give in return.

Using a template comes with another benefit. You can save time. You cut out much of the research required to craft an appropriate document by downloading a professionally researched and designed template. Rather than spending hours learning about templates and contract creation, you plug in some basic data and run a spelling and grammar check. You’ll find that using a template makes it much simpler to avoid mistakes. Then you can opt to have an attorney review your template-made contract to ensure it’s ironclad.

What Makes a Well-Written Equipment Rental Agreement

A well-written equipment rental agreement states the terms and conditions on which the renting of the equipment is agreed to by both the lessor (renter) and the lessee (renter). Thus ensuring that both parties have a clear understanding of their rights, obligations, and legal responsibilities when it comes to the equipment being rented. This document helps protect both parties if a disagreement arises and is often cited in court or other dispute mediation.

Having a legally binding and comprehensive agreement in place will help ensure that none of the parties’ obligations are exceeded or taken advantage of when renting equipment. The contract should identify who can use the equipment, who is responsible for its maintenance, how long they have access, and other crucial aspects of the agreement. In short, a well-written equipment rental agreement clarifies the exact arrangement and protects your interests and rights.

FAQs

Contracts, like equipment rental agreements, are a complex topic. Below we’ve answered some of the most frequently asked questions related to this topic to help you. You’ll learn more about the benefits of renting, renting versus leasing, types of equipment leases, and so much more.

Equipment rental refers to the process of renting out equipment, such as tools, machines, or vehicles, for a specified period. This type of rental usually involves a fee that the customer pays. Equipment rental is commonly used in various industries, including construction, hospitality, medical, and entertainment. Equipment rental can provide businesses with access to the necessary tools and resources they need without having to purchase them outright. It can also reduce costs by not buying and maintaining the equipment over time.

An equipment lease agreement is a legal document between two parties – the lessor and the lessee – that outlines the terms of a rental or leasing arrangement for commercial equipment. It typically includes details such as the duration of the lease, the monthly payment amount, any applicable taxes or fees, and any maintenance or repair responsibilities of the lessee. It may also include clauses concerning the transfer of ownership at the end of the lease term and any other conditions that both parties agree to. The agreement is a binding contract between the two parties and should be carefully reviewed before signing to ensure that all parties are protected.

Equipment leases are agreements between a lessor (the owner of the equipment) and a lessee (the party renting the equipment). There are two primary types of equipment leases: operating leases and capital leases. Operating leases are when the lessor retains ownership of the equipment throughout the lease period, during which the lessee will use it—often with maintenance services and other related service contracts included. The lessee is usually required to return the equipment at the end of the lease term. The benefit of this type of lease is that it is often less expensive than buying the equipment outright since there is no maintenance fee.

Equipment rental is an expense associated with renting equipment for a business. This could include anything from heavy machinery to office furniture and other items a company may need but not own. Equipment rental is typically tax deductible as an ordinary and necessary business expense. When classifying equipment rental in financial paperwork, it should be listed as a separate line item under the category of “rental expenses.” The rental cost should be broken down into the cost of the equipment itself, any taxes, and any additional fees or charges associated with the rental. Keeping track of all equipment rental expenses is vital, as they can impact your taxes.

Renting equipment and leasing are two different concepts. Renting involves the temporary use of goods or services, usually for a fee. Leasing is a contractual arrangement in which the owner of an asset (the lessor) provides the equipment to the user (the lessee) in exchange for regular payments. With leasing, the lessee will usually have the option to purchase the asset at the end of the lease term. Renting is typically used for short-term needs, while leasing is usually better suited for long-term needs.

Equipment leasing offers businesses several advantages over other financing options. The two major benefits of equipment leasing are cost savings and flexibility. Cost savings is one of the primary advantages of equipment leasing. When you lease, you only pay for the use of the equipment rather than the entire cost upfront. This means you can keep your upfront costs low, allowing you to free up money for other investments or to pay off existing debt. In addition, you can often deduct your lease payments from your taxable income, helping you save on taxes as well. The second significant benefit of equipment leasing is flexibility. You can use the equipment for as long as you need it without the commitment to buy, maintain or upgrade in the future.

Yes, equipment rental is an asset for businesses. Equipment rental is considered a capital asset, meaning it is an item of value owned by a company and can be used to generate income. Equipment rental is typically listed as a long-term asset on tax and finance forms, meaning it has a useful life of more than one year. Equipment rental can also be depreciated over time, which can help reduce the taxes a business has to pay.

Companies rent equipment for a variety of reasons. One of the most common reasons is to save money. Purchasing equipment can be expensive, and renting can be a much more cost-effective option. Additionally, renting equipment allows companies to access the latest technology without investing in ownership. Doing this can be especially beneficial for companies that need specialized equipment for short-term projects. Renting also allows companies to avoid the costs associated with maintenance and storage. When a company rents equipment, they don’t have to worry about the costs associated with keeping it in good working order or storing it when it’s no longer needed.

Final Thoughts

An equipment rental agreement is an essential document for any business or individual who rents out equipment. It is a legally binding document that outlines the terms and conditions of the rental and provides a framework for resolving any disputes that may arise. Using a well-written, professionally designed equipment rental agreement template saves time and ensures your contract has all the essential elements needed so you can safely loan your unneeded equipment out for a profit.