Payment Schedule Templates

A staged payment works far better when both sides can see the whole plan rather than tracking it from memory. Payment schedule templates set every payment down on its own line, with the amount, the date it is due, and what it is tied to. They span the common ways a plan is arranged, from fixed dated installments to payments released against completed work to fees billed by the hour, so the structure matches how your money actually moves.

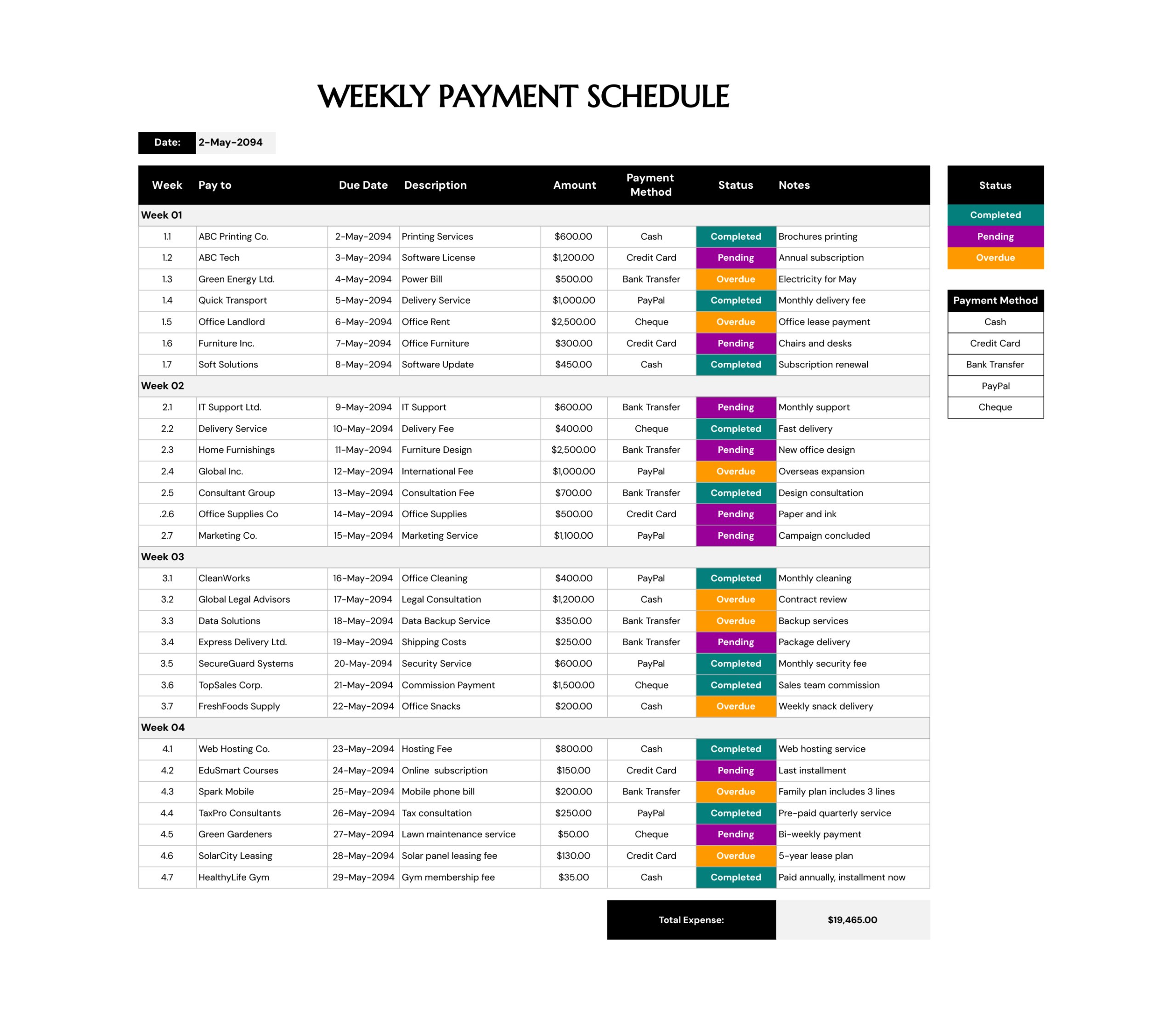

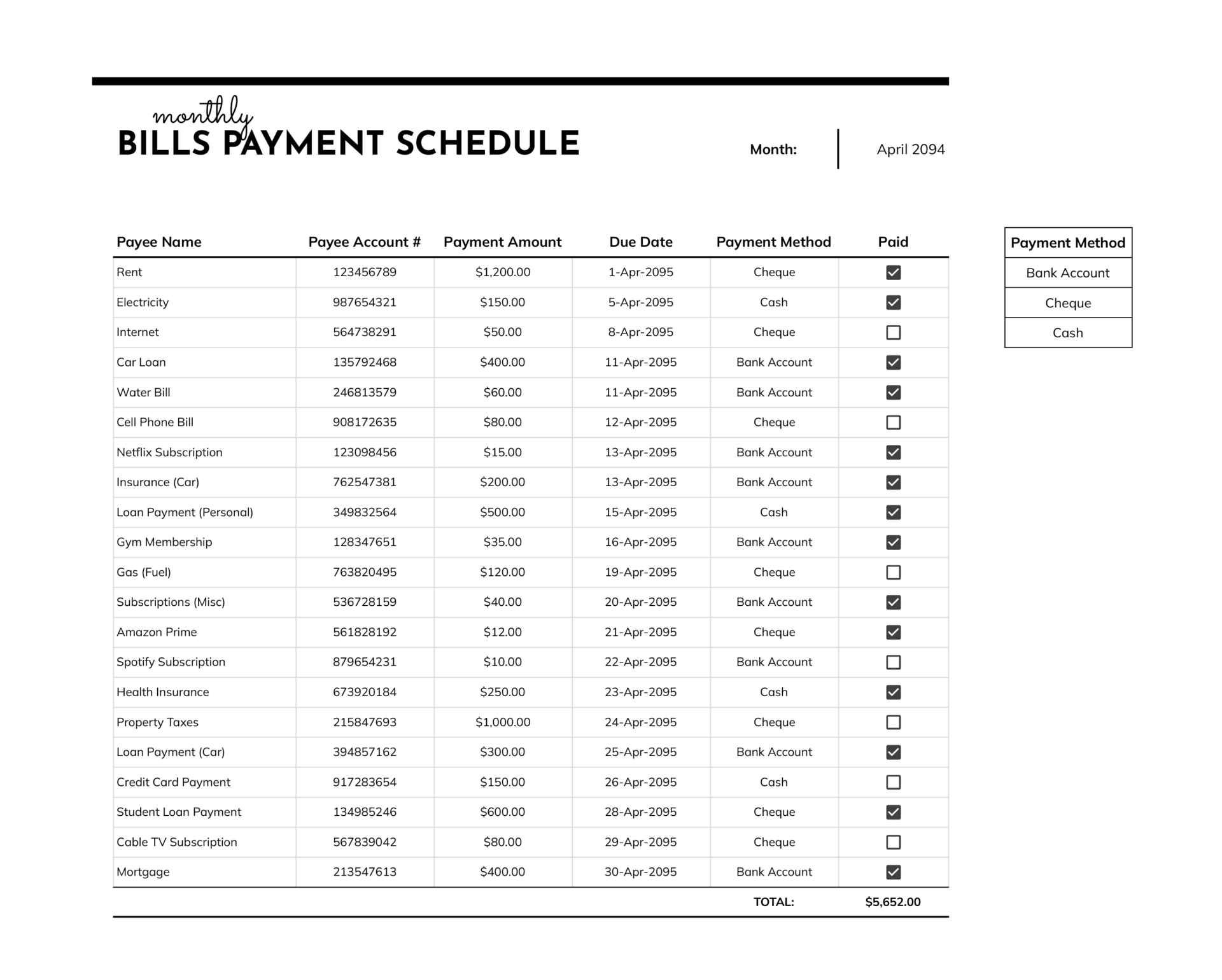

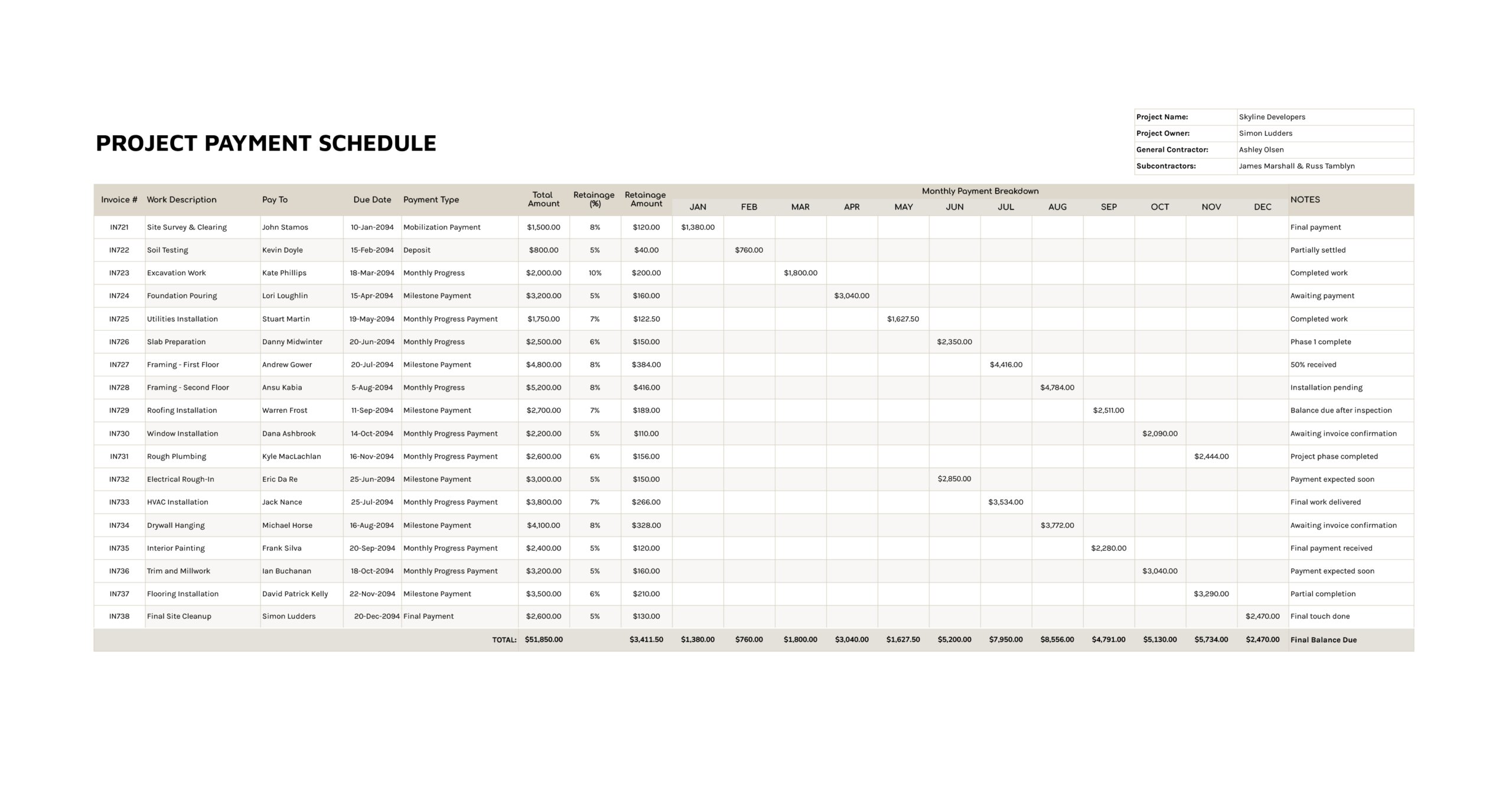

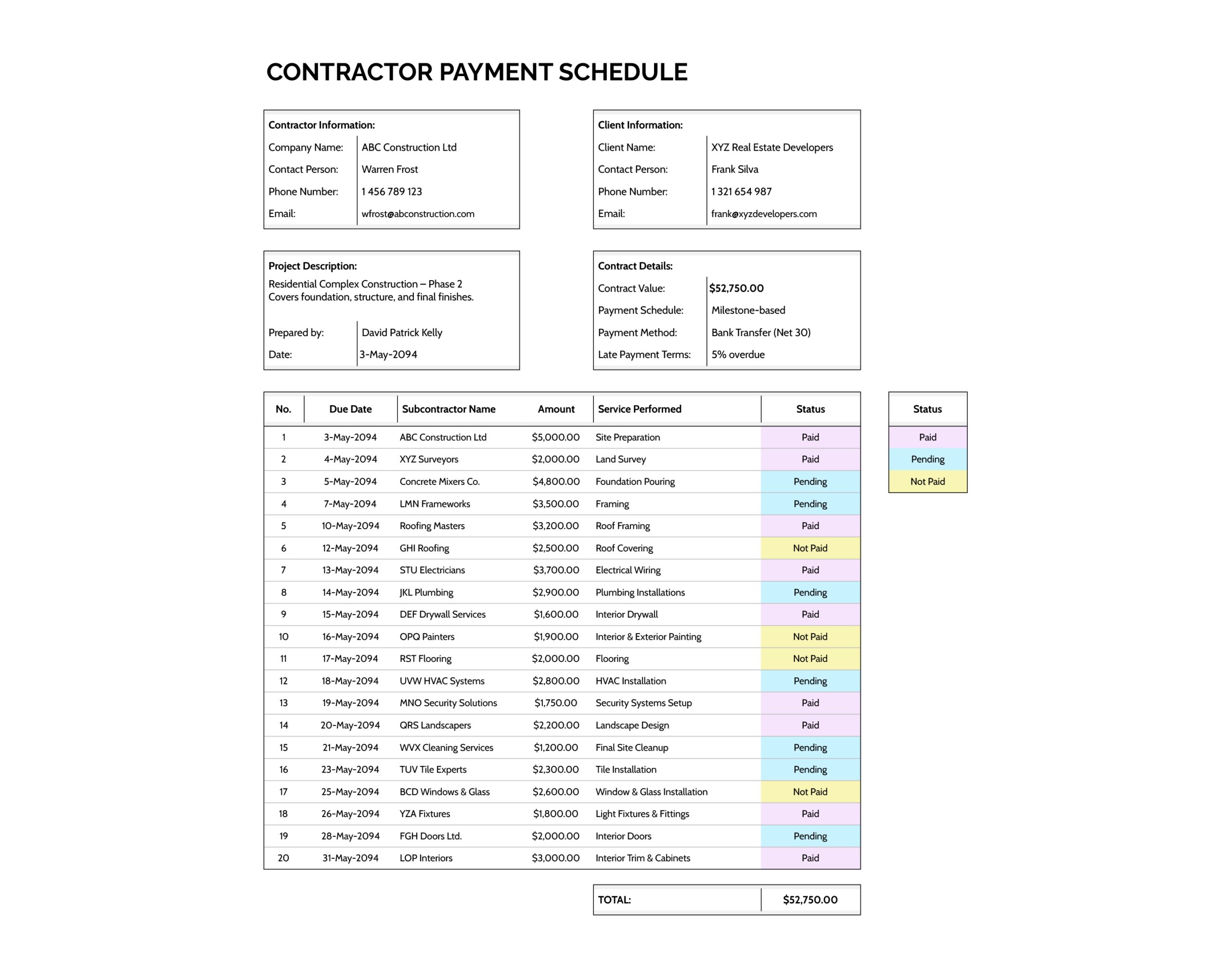

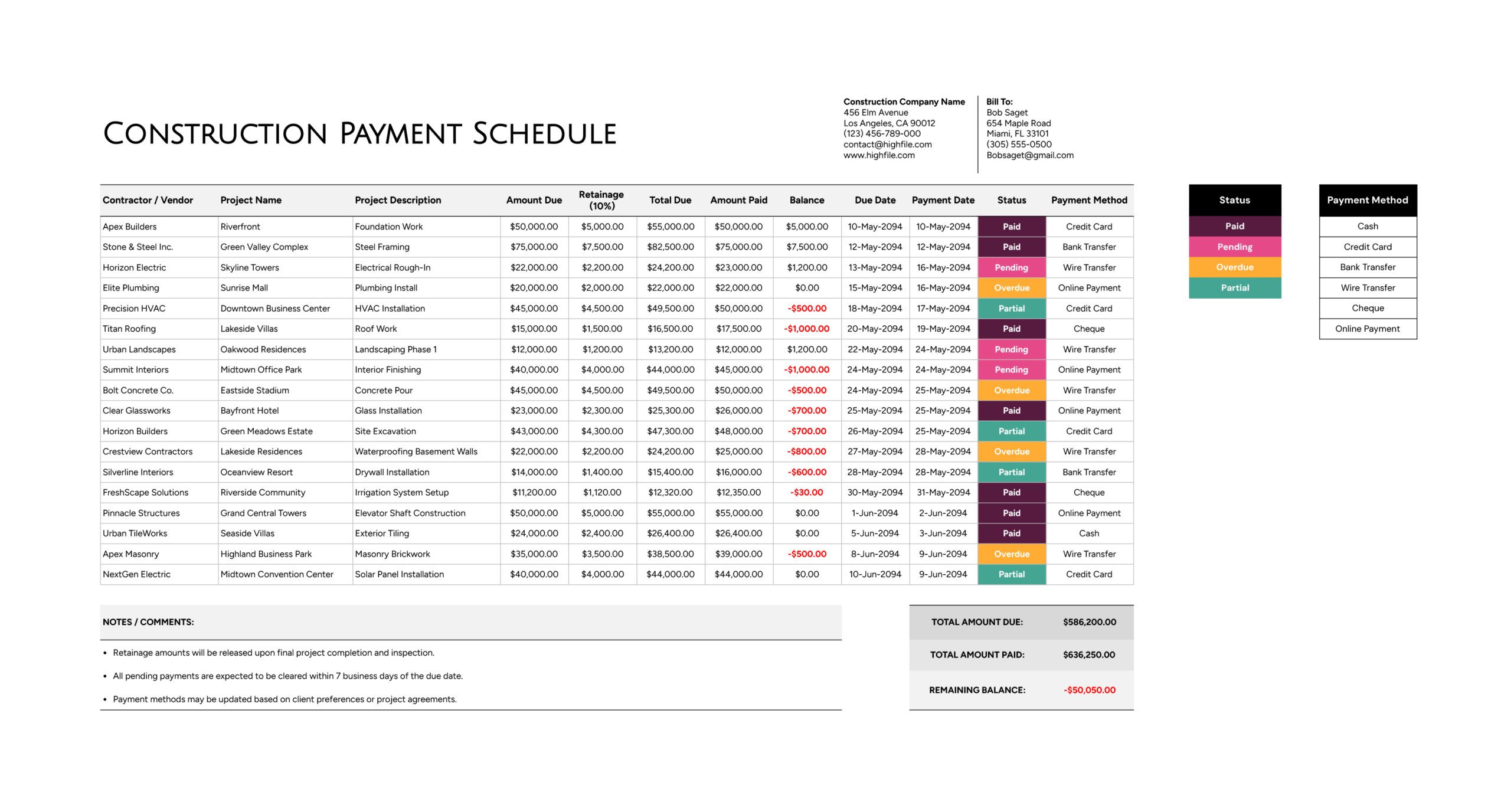

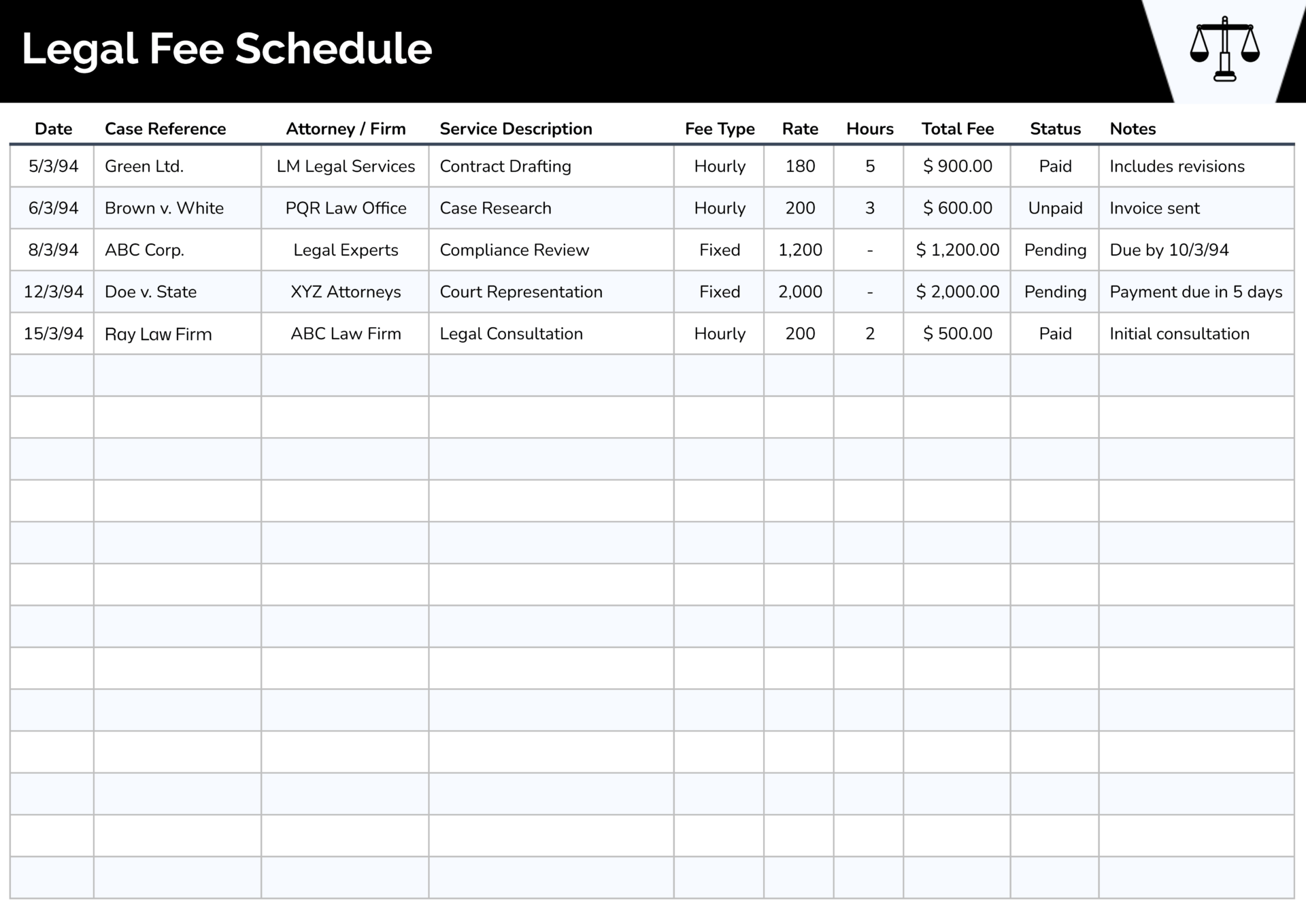

These payment schedule templates set a staged payment arrangement out in full, with every payment on its own line showing the amount, the date it is due, and what it is tied to. The payer and the payee work from one shared record instead of tracking it loosely, and a running total means the outstanding balance is clear at any point in the plan, not just at the end.

The collection covers the common ways a plan is arranged, from fixed dated installments to payments released against completed work to fees billed by the hour. Some are printable documents you complete by hand; others are spreadsheets that work out the figures and keep the balance correct as you fill them in. You set the terms of your own arrangement, the amounts, the dates, and the milestones, and the template keeps the structure and the arithmetic straight, so both sides end up with the same schedule to rely on.

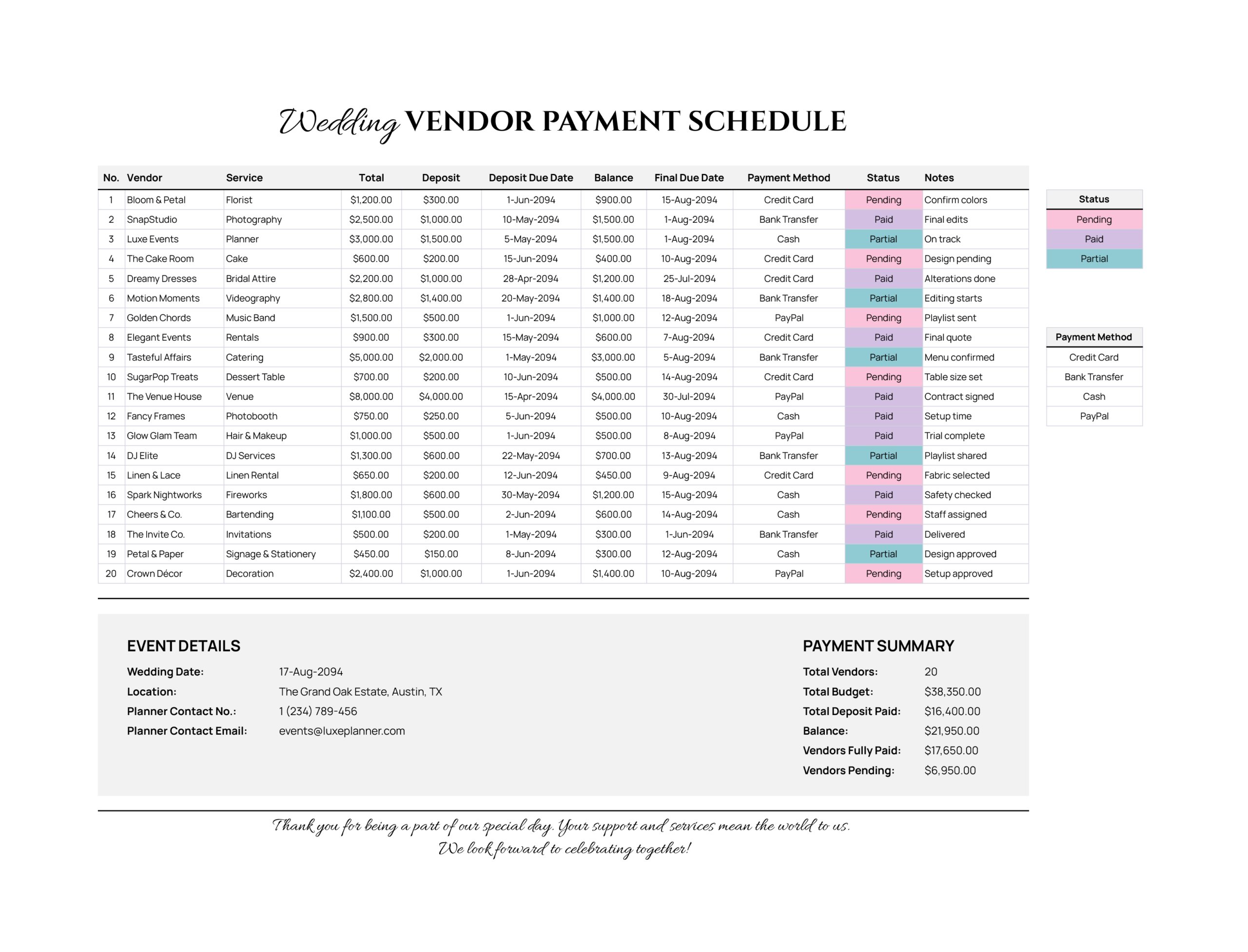

Where disputes start: On milestone-based payments, the clarity that prevents disputes is in the trigger, the specific, checkable thing that releases each payment. A schedule that ties a payment to a defined deliverable rather than a rough date is the one that stands when the work and the money have to line up.

What a payment schedule records

The parts that turn an agreement into a clear record of what is due.

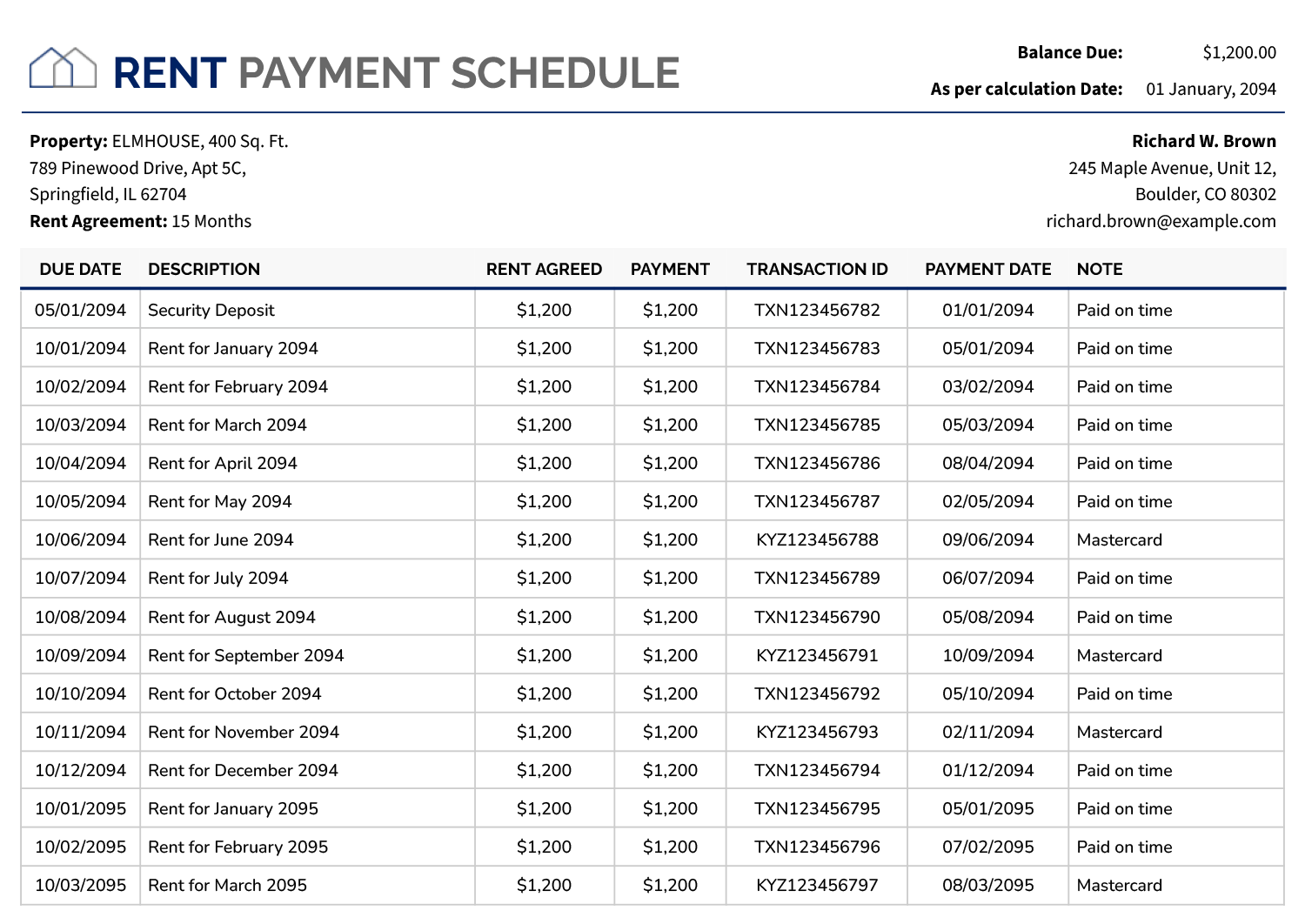

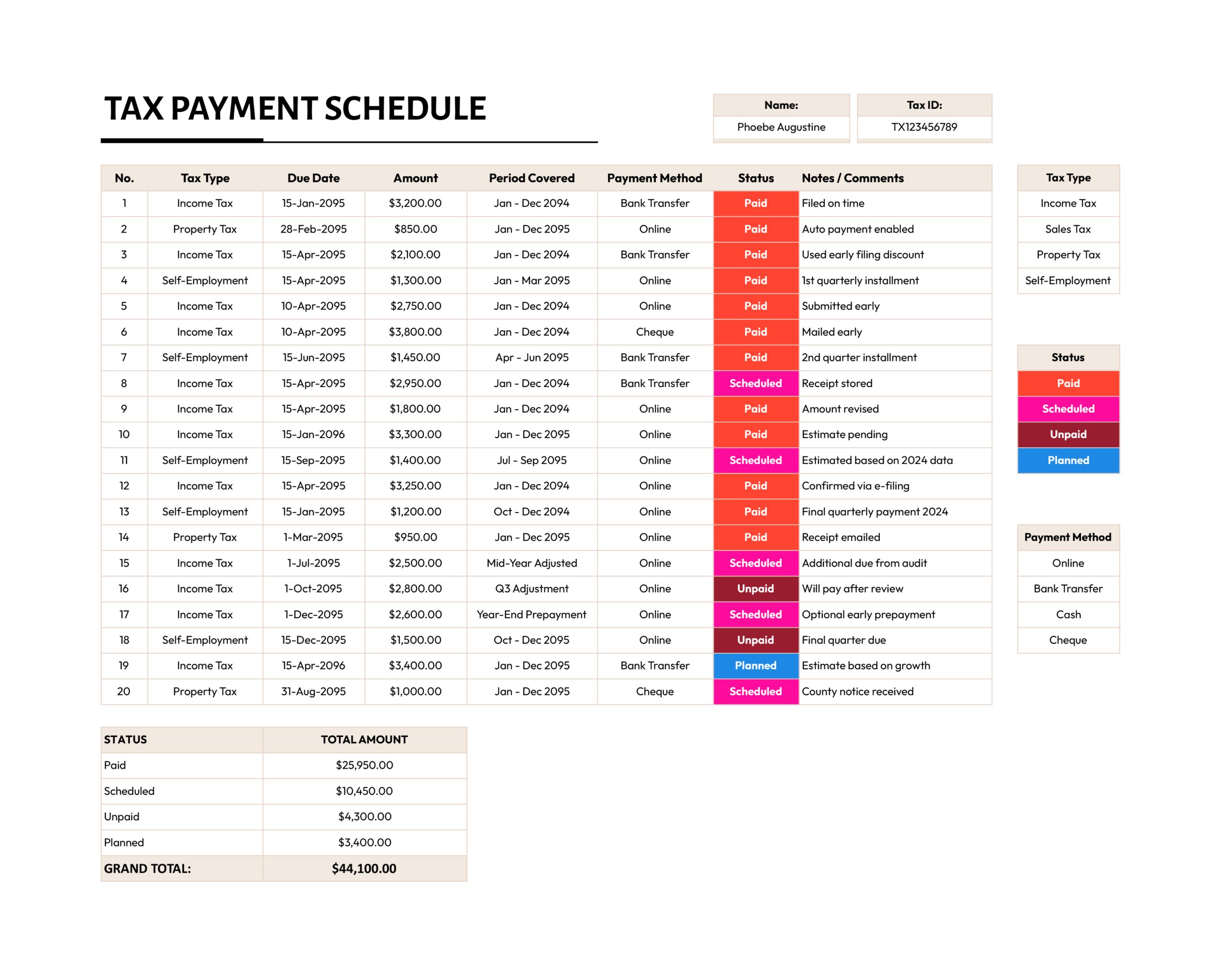

Each installment or release on its own line, so the full set of payments reads as a complete sequence rather than a running tally.

What is due and when, the core of every payment schedule and the detail both sides refer back to.

What each payment is tied to, a completed phase, a delivered item, a billing date, so a release is plainly earned rather than arbitrary.

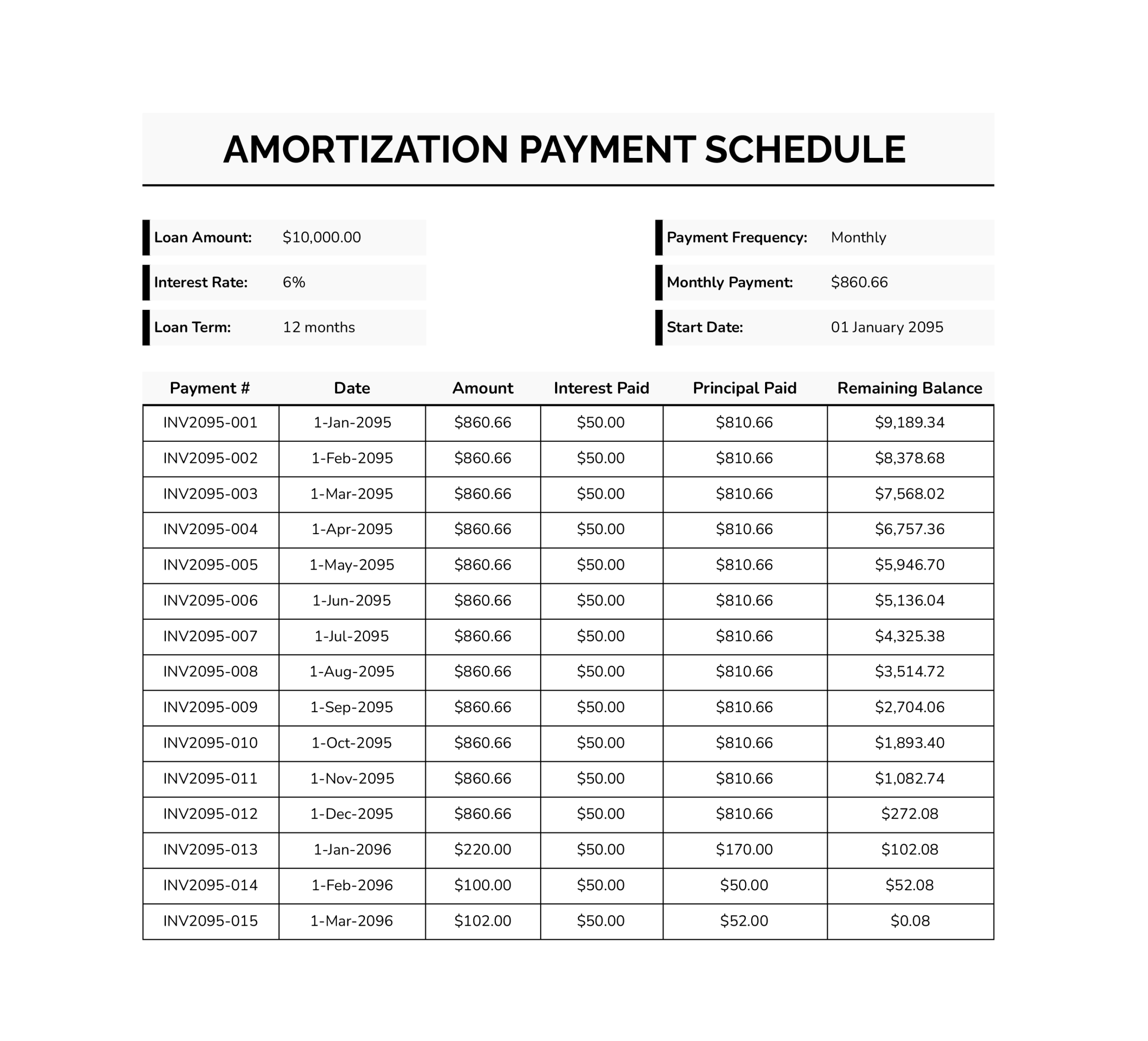

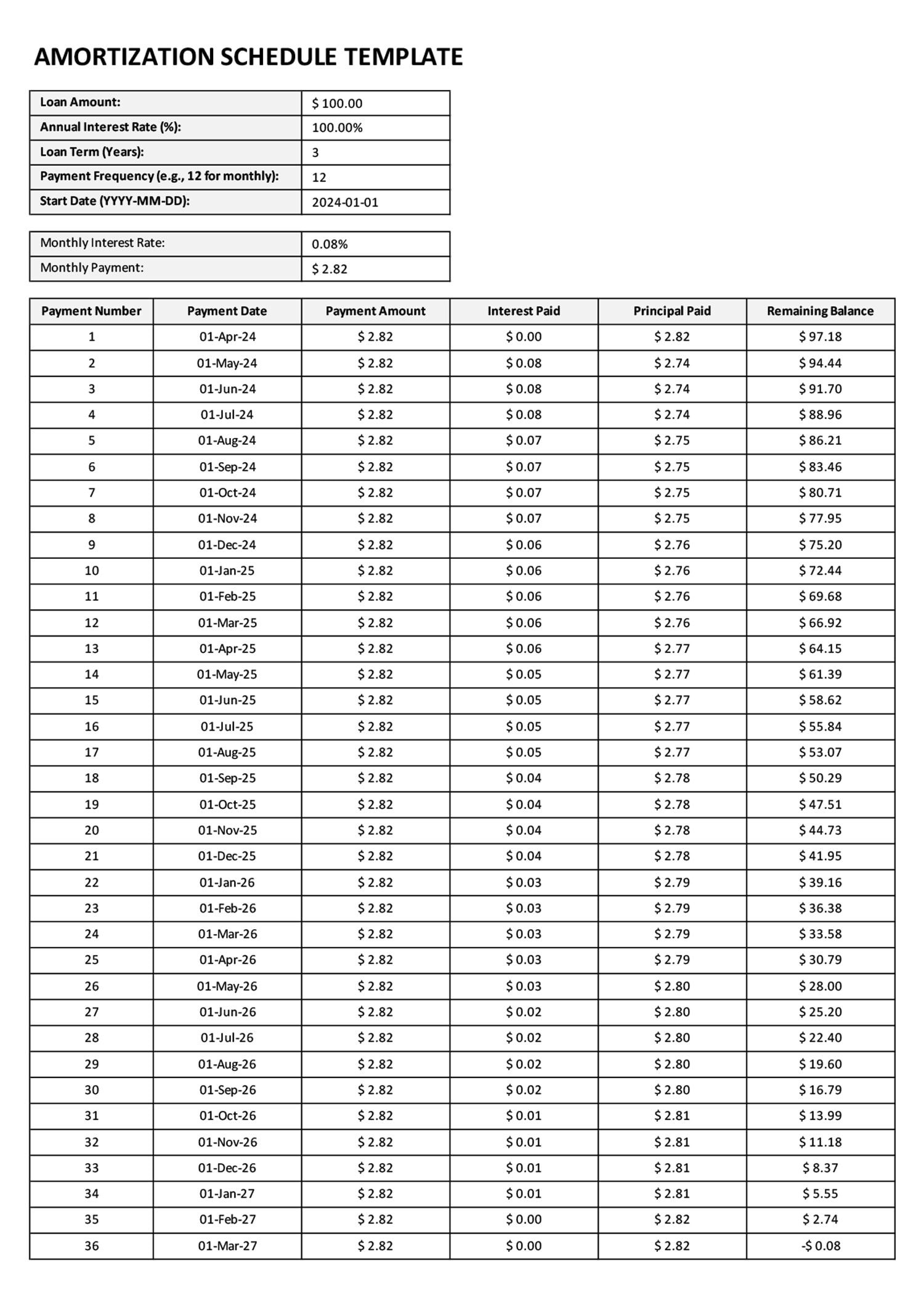

On the loan amortization version, the part of each payment that clears the debt and the part that is interest, shown separately so the cost of the loan is visible payment by payment.

The amount still outstanding after each payment, so where the arrangement stands is visible at every step, not only at the end.

On the loan amortization version, the payment, interest split, and balance worked out from the amount, rate, and term you enter, with room for extra payments.

Setting up the payment schedule

From the terms of an arrangement to a schedule both sides can rely on.

Choose a fixed-installment layout for a loan or regular plan, or a milestone-based one for staged contractor, vendor, or project payments. The structure should match how the arrangement actually pays out.

On the loan amortization version, fill in the amount, interest rate, and term, and the schedule computes each installment, the interest and principal split, and the balance. For staged work, enter the agreed amounts directly.

Tip — On the loan version you can add extra payments and see how they shorten the term and cut the total interest, so the schedule shows the effect of paying ahead rather than leaving it to guesswork.

Set the date or the trigger for each payment. For staged work, name the specific milestone that releases it, so the payment is plainly earned and not open to argument.

Confirm the payments add up to the full amount and the balance lands at zero. Where the schedule computes them this is automatic; on a manual one it is the step that catches a miskeyed figure.

FAQs

Does the loan template work out the payments for me?

Yes. The loan amortization template is built in spreadsheet form and computes each installment, the split between interest and principal, and the remaining balance from the loan amount, interest rate, and term you enter, so you set the terms and it produces the full schedule.

Can I see the effect of paying extra on a loan?

The loan template has room for extra payments and reflects how they shorten the term and reduce the total interest. It shows the minimum against paying ahead, so you can compare the two before committing to either.

What is the difference between an installment and a milestone schedule?

An installment schedule pays fixed amounts on set dates, like a loan; a milestone schedule releases payment when a defined piece of work is done, like a contractor draw. The collection covers both, since which one fits depends entirely on the arrangement.

How do milestone payments avoid disputes?

By tying each payment to a specific, checkable trigger rather than a rough date. When a release is linked to a defined deliverable, both sides can agree it has been met, which is what keeps the work and the money lined up.